Updated April 4, 2023

Raymond Micaletti, Ph.D.

Macro Money Monitor

Risk happens fast in financial markets. While some trends take months or even years to play out, such as the Federal Reserve’s rate-hiking cycle that began in the first quarter of 2022, the failure of SVB Financial (SIVB) unfolded in just a few days.

It was an old-fashioned run on the bank driven by speculation and fear that the private equity and venture capital-focused financial institution would be unable to pay back all its depositors.

SIVB’s balance sheet, or the assets it owns and liabilities it owes, was also in a sketchy condition that few analysts, regulators, or even risk officers at the California-based firm knew about. The result was that its share price plunged from as high as $348 in early February to likely being worth zero today.

SIVB Stock Price History: From $763 to Potentially $0

Source: Stockcharts.com

So, what caused the bank run, will it keep happening, and what does it mean for the broader economy and stock market? Let’s dig into the details to gain a better understanding of where things stand and review how and why Allio eliminated its exposure to the broad U.S. stock market and tech stocks in advance of this house of cards falling.

Shades of 2008

It was a wild weekend that had echoes of the 2008 Great Financial Crisis (GFC) with a bit of the year-2000 dot-com bust mixed in. Regulators from the Treasury Department, Federal Reserve, and FDIC announced on Sunday, March 12, shortly before stock market futures trading commenced, that all depositors at SIVB would be protected.

Another major financial firm, New York-based Signature Bank (SBNY), was closed over that weekend, too.

The policymakers crafted a new liquidity facility called the Bank Term Funding Program (BTFP). The emergency lending program basically guarantees that bank holdings would be valued at par so that depositors can be repaid.

2023 So Far: Two Bank Failures, $319 Billion in Assets Affected

Source: FDIC

Understanding FDIC Limits

Immediately, scrutiny was cast on the emergency measures as being akin to a bank bailout. That’s arguable, but the aim is to protect depositors from losing their savings. The FDIC insures deposits up to $250,000 per depositor, per insured bank.

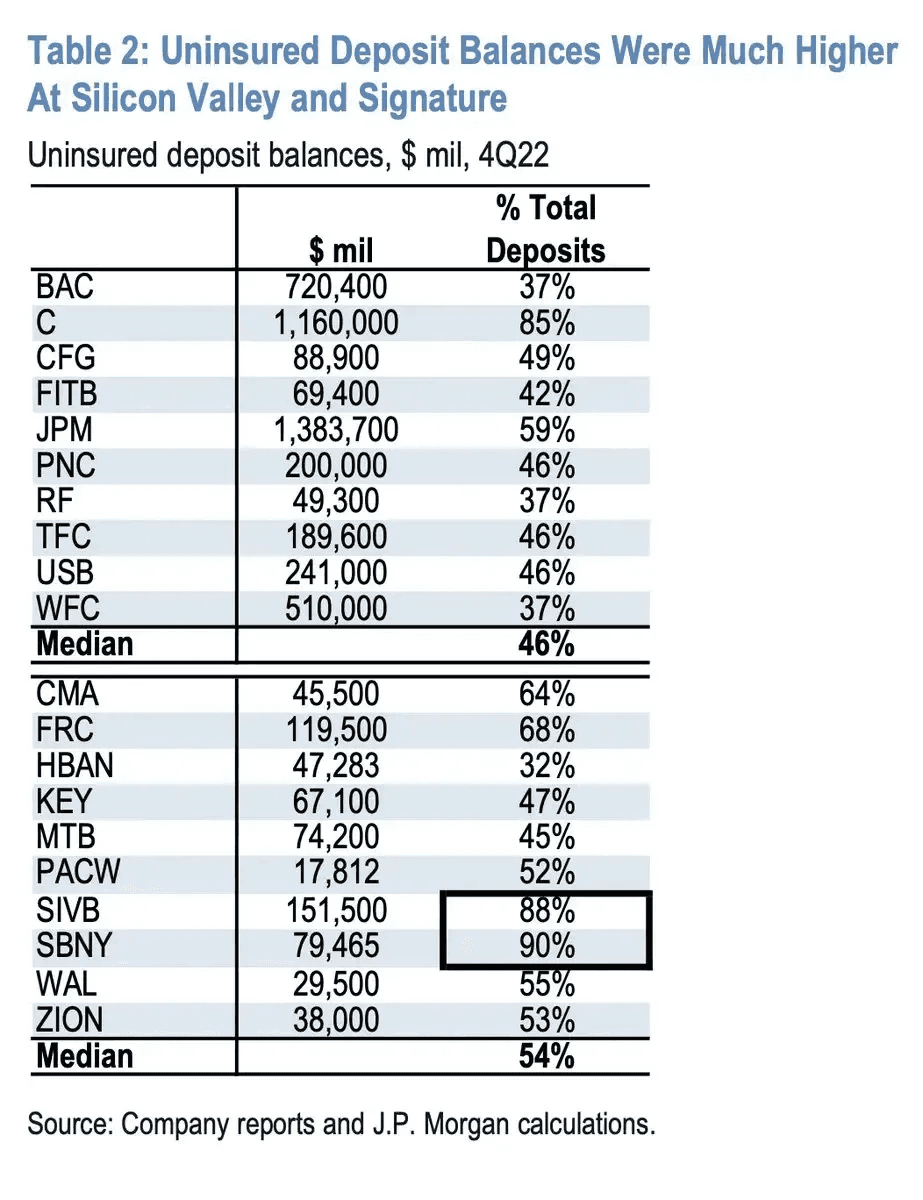

One of the problems with depositors at SIVB (among other regional and larger banks) is that individuals and businesses held cash savings well in excess of that limit, thus a firm such as SIVB had upwards of 90% of total deposits above FDIC limits.

SIVB Is Not the Only Nefarious Player

SBNY was in the same camp. As a result, when fear creeps in that a bank will be unable to repay depositors, withdrawals ensue at a rapid clip due to the level of uninsured deposits. For this reason, the consortium of regulators announced a backstop – not for the executives, shareholders, or creditors of banks, but for the customers. The “bailout” is really for customers who knowingly held deposits more than the FDIC-insured limit.

SIVB & SBNY Had High Uninsured Deposit Balances

Source: J.P. Morgan

But let’s go back in time. How did this private equity (PE) and venture capital (VC) bank unraveling come to pass? Well, like so many wild events in the last few years, we can trace it back to the COVID-19 pandemic.

In March 2020, the world was put to an instant halt. Central banks around the world and legislators took swift action to inject enormous amounts of monetary and fiscal stimulus into the markets. Even after the worst of the strict lockdown measures of 2020, the U.S. Federal Reserve and Congress kept pumping liquidity into the system. We all know what unfolded by late 2021 through today: inflation.

From Boom to Bust

There was simply too much money supply growth and much of it went into the stock and bond markets, driving up equity prices and pushing bond yields lower. The Fed kept interest rates near 0% for too long, and that made the cost of borrowing for highly risky activities nearly free.

Niches that received massive capital and speculative investment dollars were the domestic venture capital and private equity spaces, primarily located around Silicon Valley. SIVB’s filings show that quarterly VC investment dollars more than doubled from 2020 to a peak in Q4 2021. By the first quarter of this year, though, VC investing had slowed sharply.

SIVB benefitted from a huge influx of deposits during the boom time. According to FactSet, from the end of 2020 through Q1 of 2021, total deposits rose 94%, much of that stemming from the risky VC area (which included customers with deposits above the FDIC insurance limit). And like any good bank, it lent out money to its customer base or invested in longer-duration securities. This is where things turned south for the California-based regional bank.

Rising Interest Rates Caused Unrealized Losses

Instead of extending large amounts of credit to would-be borrowers, SIVB purchased significant amounts of mortgage-backed securities (MBS). If you’ve seen “The Big Short,” you might be familiar with the term. They are typically relatively safe assets, but in contrast to the GFC, instead of large defaults hitting, it was interest rate risk that reared its head.

Massive Unrealized Losses on Banks’ Books Via Held-to-Maturity Assets

Source: FDIC

As rates rise, the value of bonds goes down. Moreover, the longer the maturity of fixed-income assets, the greater the negative impact of higher rates. Owning “long-duration” bonds in a rising interest rate regime is bad news for a bank. And how the accounting treatment worked did no favors for SIVB.

Accounting Treatment Temporarily Masked Emerging Problems

You may have heard of the terms “available for sale” and “held to maturity” as it pertains to SIVB’s balance sheet. Much of SIVB’s assets were marked as the latter, which, as opposed to trading securities, meant that gains and losses on such positions were not marked on the books until they were sold. That’s all fine during normal times, but when depositors demand their cash, the bank is forced to sell securities to meet the obligations. That means selling assets that were primarily bonds that had declined in value due to rising interest rates and recognizing losses on the income statement.

Held-to-Maturity Assets: Gains and Losses Not Marked Until Sold

Source: Reynolds Center for Business Journalism

SIVB, and apparently other regional banks, did a poor job of a key risk management activity for any bank: asset-liability matching (ALM). Good corporate governance includes protecting a company from obvious areas that could put the company out of business.

For a bank, priority one is ensuring that the liability side of the ledger is protected enough by the asset side. SIVB failed miserably at that first-principle, though complex, ALM task. Shockingly, it’s reported that the bank had no chief risk officer for eight months during 2022.

A Failed Capital Raise Spooked Investors

Perhaps the death knell came in early March when SIVB attempted to raise capital by offering common stock and preferred shares to help offset losses from the sale of its available-for-sale securities after it had previously disclosed more than $90 billion in held-to-maturity assets. The stock plunged on the news that it essentially needed more money to stay solvent.

The selling cascade led to a crash of other regional bank equities, and the overall stock market endured its worst week of the year. By the weekend, depositors lined up at small and mid-sized banks across the country fearing their cash would be at risk.

Financial Conditions Tighten Sharply Post-SIVB Collapse

Source: Bloomberg

Putting It All Together

Are you connecting the dots? COVID stimulus measures, including the Fed’s zero interest rate policy, brought about massive speculation in the tech and VC spaces, boosting SIVB’s bottom line for a time. Its share price soared, and executives at the bank were no doubt on cloud nine in 2021. The party lasted too long, and the music was about to stop. The fundamentals of SIVB’s business were cooked by early 2023, and few analysts, investors, and regulators noticed.

A failed capital raise brought down the stock price just as the crypto-focused Silvergate Capital was collapsing, then depositors panicked, withdrawing a stunning $42 billion by the close of business on Thursday, March 9. The result was the largest bank failure since the GFC, and confidence in the overall financial system was once again called into question.

What took four decades to build was brought down in less than two days at “Silicon Valley Bank.” Ironically, technology and the ease of transferring cash today played a key role in the bank run.

Looking Ahead, Identifying Risks

Going forward, small business banking may be tougher, tech-led investment dollars could be fewer, and the overall Financials sector is back in 2008 fear mode, wondering when the next shoe may drop.

The good news, arguably, is that depositors are protected given the fast policies inked. Still, there will be strains on the financial system. The right investment risk management approach is needed to navigate this volatile environment.

How We Allocated in Advance of the SIVB Downfall

Did Allio see it all coming? We do not claim to have the crystal ball to have foreseen the swift SIVB bust, but our global macro investment team saw the broader writing on the wall. As the Fed hiked interest rates at the fastest clip in more than four decades, we knew something would break in the economy before long, and that it would likely be in the spec-heavy and rate-sensitive technology sector.

As part of our strategic approach to asset allocation, we took our exposure to broad-market U.S. equities and tech stocks to 0% despite tech being the largest weighting in the S&P 500. We are not afraid to go our own way when we deem it appropriate.

And while SIVB is in the Financials sector, it was the tech space that drove the bank’s business. A freeze in the PE and VC markets, rooted in the Fed’s fast credit tightening endeavor, led to the party lights turning off and the bank's doors being shuttered.

The Bottom Line

We are constantly on the hunt for what could go wrong in the global investment markets. While we believe that long-term investing in stocks is the best path to building wealth and becoming financially independent, there are corrections, bear markets, and even crashes along the way. It takes the right global macro portfolio centered on risk management to navigate volatile times like today.

Allio’s team of hedge fund veterans closely monitors trends and events such as the SIVB collapse so that investors own portfolios that are strategically aligned with their goals and risk tolerance. We use full-scale optimization with machine learning to meet the complex, inflationary market conditions of our time.

Want access to your own expert-managed investment portfolio? Download Allio in the app store today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.