Updated March 7, 2023

Raymond Micaletti, Ph.D.

Alpha

In last week’s commentary, we mentioned we were looking for a pullback in the dollar and a bounce in equities.

In the early part of last week, the dollar cooperated, falling approximately 1% (a decent-sized move for a currency). But equities refused to join the party–despite several valiant attempts to rally–seemingly held back by interest rates pushing to their highest levels since the fall.

Thursday’s economic data didn’t help matters, as productivity numbers came in well below expectations while labor costs were materially higher than estimated–raising the specter of an entrenched wage-price spiral.

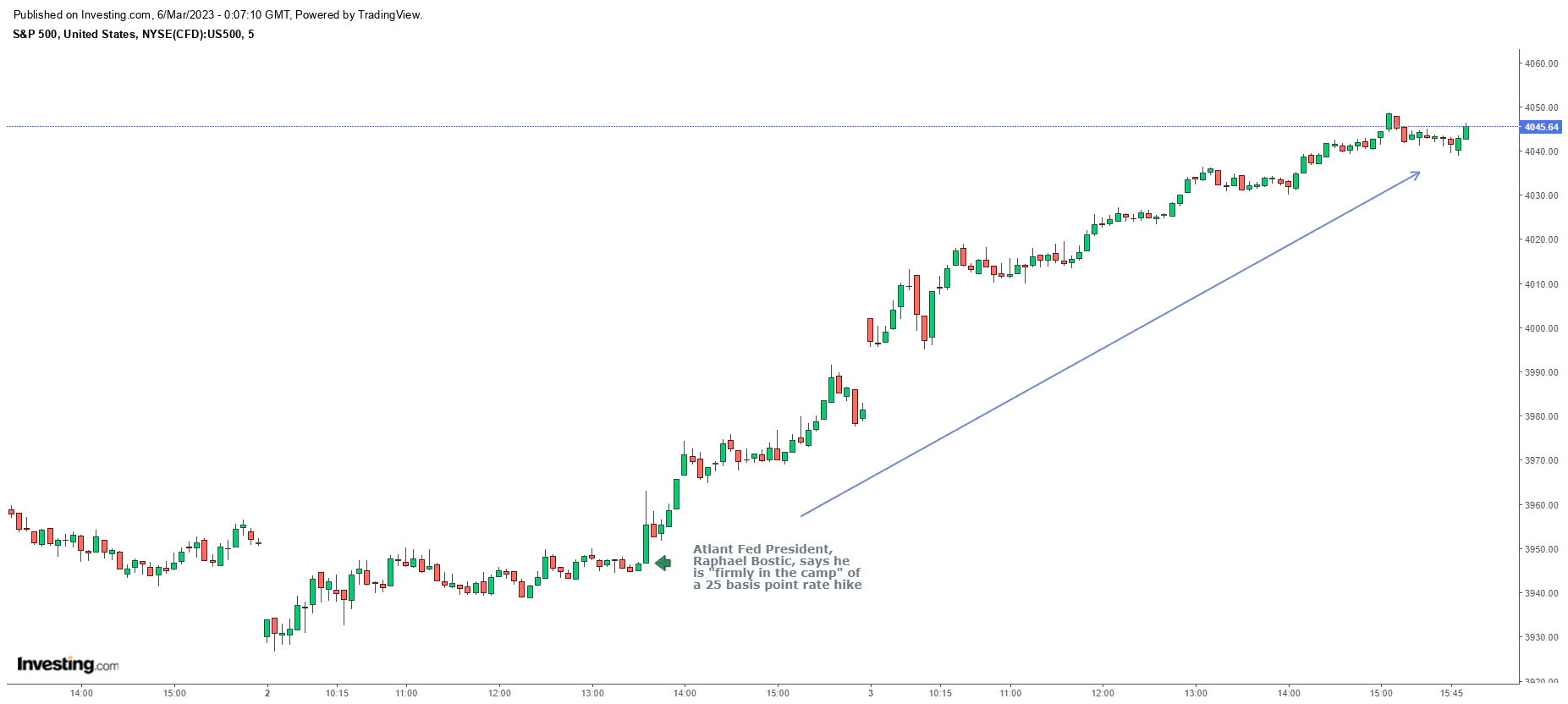

Initially, equities didn’t take the Thursday data well. The S&P 500 fell as low as 3925 that morning, 6.7% below its intraday high on February 2nd.

But, as so often happened last year when equities looked to be in danger of falling into the abyss, the Fed came to the rescue. This time it was Atlanta Fed President, Raphael Bostic, on Thursday afternoon who calmed the market’s nerves by saying he was “firmly” in favor of a 25 basis point rate hike at the next Fed meeting (March 22nd).

When that news hit the market, equities took off like a rocket and barely looked back, rallying nearly 3% from Thursday afternoon into Friday’s close.

S&P 500 performance before and after the Atlanta Fed's 3/2/23 comments | Source: Investing.com

For the week, U.S. equities were up 2%, while the dollar fell 0.5%. For those bullish equities, the strong bounce off technical support (delayed though it may have been) was heartening. It suggests the rally off the October lows might still be in progress.

By far the most interesting data point to us, however, was the Fed stick-save–yet another instance where the Fed has talked hawkishly when equities are at multi-month highs (over 4000) and dovishly when equities appear in need of a lifeline.

This repeated pattern suggests to us that the Fed doesn’t want equities to crash or soar.

Crashing equities would likely preempt their rate hiking cycle, worsen U.S. fiscal deficits via lowered tax receipts, and as a result blow up the bond market.

Soaring equities would loosen financial conditions and make inflation that much harder to tame (and thus blow up the bond market from higher-for-longer interest rates).

The Fed appears stuck.

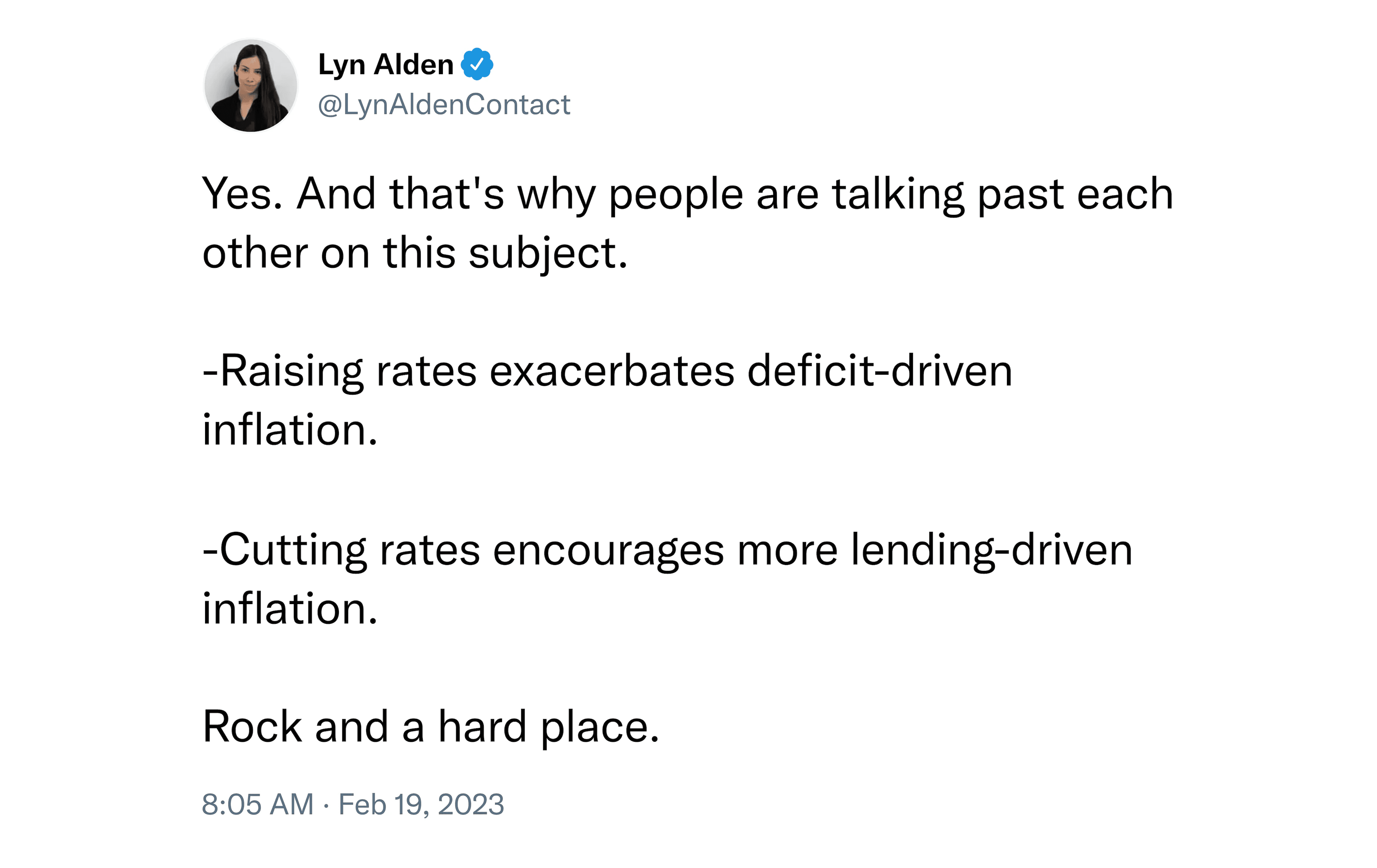

Several commentators have noted that the Fed raising rates has led to bigger budget deficits, which have led to more inflationary spending into the economy–nearly $600 billion worth of additional interest payments to bondholders–on par with past quantitative easing and fiscal stimulus episodes.

Lynn Alden summed it up well on Twitter:

If the Fed truly is between a rock and a hard place, with bond market turbulence almost a certainty, it probably does not want to inflame equity markets unnecessarily at the same time (especially as we get closer to the 2024 election cycle).

Thus, we might expect equities to trade in a range that slowly drifts higher (right now that range appears to be somewhere between 3900 to 4300 on the S&P 500).

From a positioning perspective, we got another installment of the Commitments of Traders Report dated to the second week of February (still three weeks delayed). At that time, the smart money was still selling the dollar strongly and was beginning to sell equities into the early February highs (but not enough to flip relative sentiment anywhere near bearish). The smart money also repositioned itself in a bullish way for non-U.S. equities (after having turned temporarily bearish).

One interesting development was that commodities stopped going down last week. Consequently, commodities sentiment rebounded into a zone that tends to have beneficial effects for equities.

The commodities rebound also suggests that the “growth scare” we warned about last week may not materialize. Indeed, reports indicate China is going all out to stimulate its economy and that will likely have global implications (China’s PMI readings have recently reached their highest level in more than a decade).

The Bull Case

The bull case for equities is that growth is picking up, earnings have bottomed (as have profit margins), and inflation has peaked. With institutions still more relatively bullish equities and bearish the dollar than retail traders, the historical odds appear to favor a continuation of the rally off the lows.

The Bear Case

The bear case for equities is that valuations imply meager long-term equity returns (~3% annualized). As a corollary, a big disconnect exists between price-to-earnings multiples and the level of real interest rates.

Our Opinion

We continue to lean toward the bullish case for equities. The combination of institutional positioning, a potential reignition of global growth, and the apparent desire of the Fed not to see equities suffer, suggests to us that equities may continue to grind higher within an upward sloping channel for the next few months.

Given the potential for inflation to remain sticky and the difficulty the Fed will have in keeping rates higher for longer without causing a crisis, we believe real rates will eventually have to turn negative, which will make equities (particularly energy stocks), gold, and commodities particularly attractive while making long-duration bonds virtually uninvestable. Consequently, our portfolios are tilted heavily toward the former and away from the latter.

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.