Updated June 27, 2023

Raymond Micaletti, Ph.D.

Alpha

The broad equity indices had modest pullbacks last week (on the order of 1.5%-2%). But given the intensity of the recent runup, those pullbacks barely registered.

Someone tweeted that the Nasdaq 100 just had its third best 30-day performance since 1984.

Bank of America noted the Nasdaq’s rolling 3-month Sharpe ratio touched 7 this past week.

And the S&P hadn’t had a weekly loss more than 80 bps since the week of March 10.

Thus, a 2% pullback on a 36% YTD return (for the Nasdaq 100) is a mere papercut.

But next week is a new week and things are starting to get interesting under the hood.

As Goldman Sachs flow strategist, Scott Rubner, put it:

“Bottom Line: Sentiment is no longer bearish – it is greedy. Investors are no longer short – they are long. Retail traders are back, liquidity is currently robust heading into the summer, pension rebalancing, corporate repurchase blackout, change the flow-of-funds picture. It will be harder from here. Those investors who will be stopped into the market have been stopped in already at this point.”

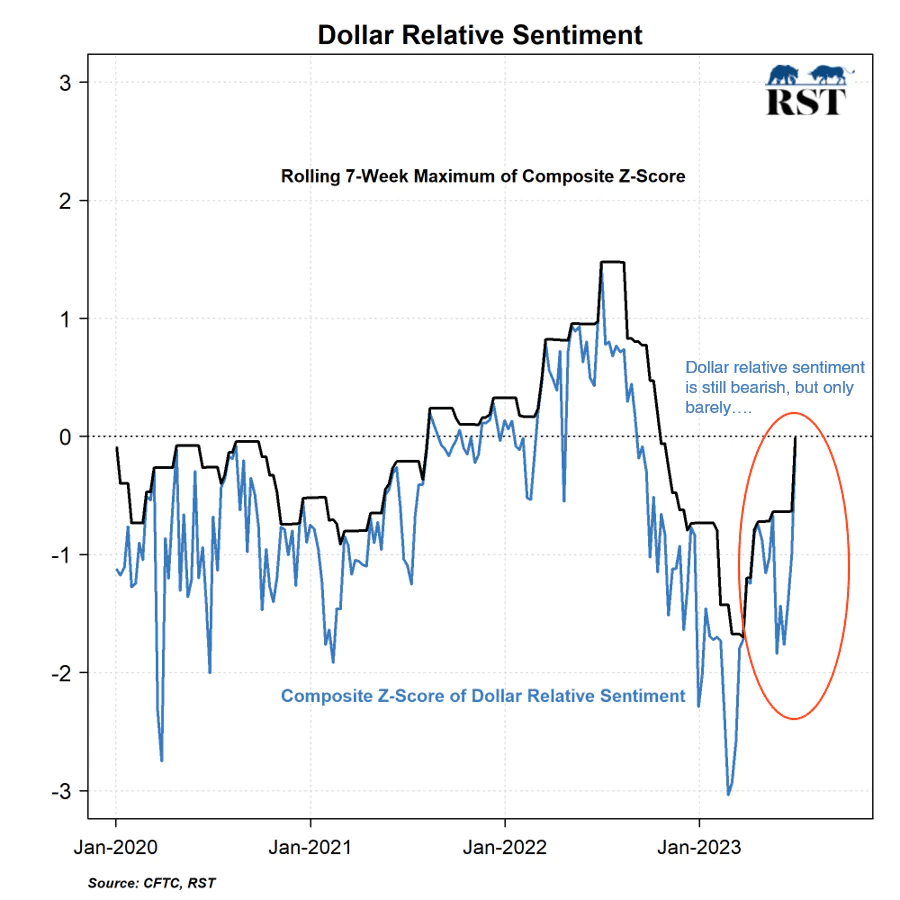

On the positioning front, the big news from last week was that the smart money in the dollar used the dollar selloff from the prior week to buy the dip in size. Dollar relative sentiment is now a hair’s breadth away from turning bullish. While it’s possible it could turn back down (without turning bullish), that seems unlikely.

Source: Relative Sentiment Technologies, LLC

If dollar relative sentiment were to turn bullish (and we expect it will), that would almost certainly have non-trivial effects on a wide range of assets–just as its turning bearish in mid-October helped jumpstart the equity rally from the October lows.

Perhaps corroborating the smart money’s buying of the dollar, institutions again sold equities last week, dropping their equity-positioning z-score further into negative territory at -0.25. Markets don’t seem to put in meaningful tops, however, until that z-score is at or beyond -2. So, there’s still some ground to cover in that regard.

Source: Relative Sentiment Technologies, LLC

Indeed, other measures of equity relative sentiment indicate equities could have up to five more weeks of supportive positioning. Which again suggests a market top is not imminent.

Notably, the Nasdaq continues to have the most supportive relative sentiment positioning both on a standalone basis and relative to the S&P 500 (and Russell 2000). Thus, its year-to-date outperformance, as extreme as it has been, may persist.

Positioning in gold has firmed up a bit and is now in a state that has been modestly supportive of gold in the past. Thus, we may see gold (which fell 2% last week as the dollar climbed 0.7%) attempt a rebound in the (potentially small) window of time before dollar relative sentiment turns bullish.

Last week, we mentioned that energy and commodities–which have struggled–may be on the verge of seeing a market rotation given the shunning of energy stocks and the U.S.’s need to refill the Strategic Petroleum Reserve.

Yet, the relative sentiment relationships that drive energy and commodities are giving no indication a rotation may be near. Thus, we may continue to see sideways or lower churn in those markets until investor positioning becomes more favorable.

Tying those all together, we have: bearish positioning in energy and commodities, soon-to-be bullish positioning in the dollar, a firming in gold’s positioning, and institutions selling equities.

Is the market suggesting a second-half credit crunch?

The Bull Case

The bull case for equities is narrow, but not necessarily weak. It rests on the market’s current technical strength and the residual effects of prior positioning and earlier breadth thrusts. Societe Generale also argues there is room for P/E expansion if the AI boom trades similarly to the dotcom boom (though the other side of that expansion might not be pleasant).

The Bear Case

The bear case for equities is gaining steam. We have:

Stretched (although not extreme) positioning

Potential end-of-month pension-fund rebalancing between equities and bonds given the large outperformance of equities

Contracting bank lending, Fed liquidity rolling over, junk bond defaults soaring

A meme stock frenzy—recent trading volume in meme stocks is in the 99th percentile of the last five years (according to Goldman Sachs)

85% of corporations will be in the blackout window for stock buybacks by the end of this week (thus removing that bid from the market)

The aforementioned changes in investor positioning across the dollar, equities, gold, and commodities

Our View

Things are starting to get interesting. For what seemed like an eternity, institutions were stubbornly bullish while speculators and retail investors were stubbornly bearish. Now that’s no longer the case.

Institutions are selling equities (to retail and speculators) and the smart money is buying the dollar. So, it’s reasonable to believe that at some point in the not-too-distant future we will get a change in trend.

Whether that change in trend comes several weeks from now (perhaps after a blowoff top in the market) or more immediately with a continuation of last week’s pullback is more difficult to ascertain.

Whereas institutions tend to be more timely with their buying when it comes to calling market bottoms, when it comes to timing the top with their selling, they often sell too early and the market continues to drift higher.

We tend to come down on the side that the market will continue higher (even if we get a near-term pullback) and we may even get a blowoff top, primarily because:

Several of the mega-cap tech stocks appear to have unfinished business on the upside (gaps to close, technical patterns to fulfill, etc.)

Investor positioning in equities likely won’t turn bearish until the end of July

Across all equity indices, sectors, regions, and countries, the Nasdaq 100 has the most bullish relative sentiment configuration of all

Animal spirits are revved up and the lack of any material pullback (so far) only serves to foment those spirits

So far, this rally is adhering to the age-old playbook: Institutions bought equities when the narrative was uniformly bearish (H2 2022) and are now selling equities when the narrative has become almost uniformly bullish.

Institutions likely have more selling to do before equities peak, but the fact they are selling suggests we may be closer to a top than a bottom–in either time or price or both.

Allio Portfolio Updates

No changes to Allio’s portfolio last week. We will continue to evaluate tactical opportunities and incorporate the aforementioned evidence of a potential credit crunch into our strategic forecasts.

Want access to your own expert-managed investment portfolio? Download Allio in the app store today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.