Updated October 2, 2023

Adam Damko, CFA

The Piggy Bank

THE MARKETS

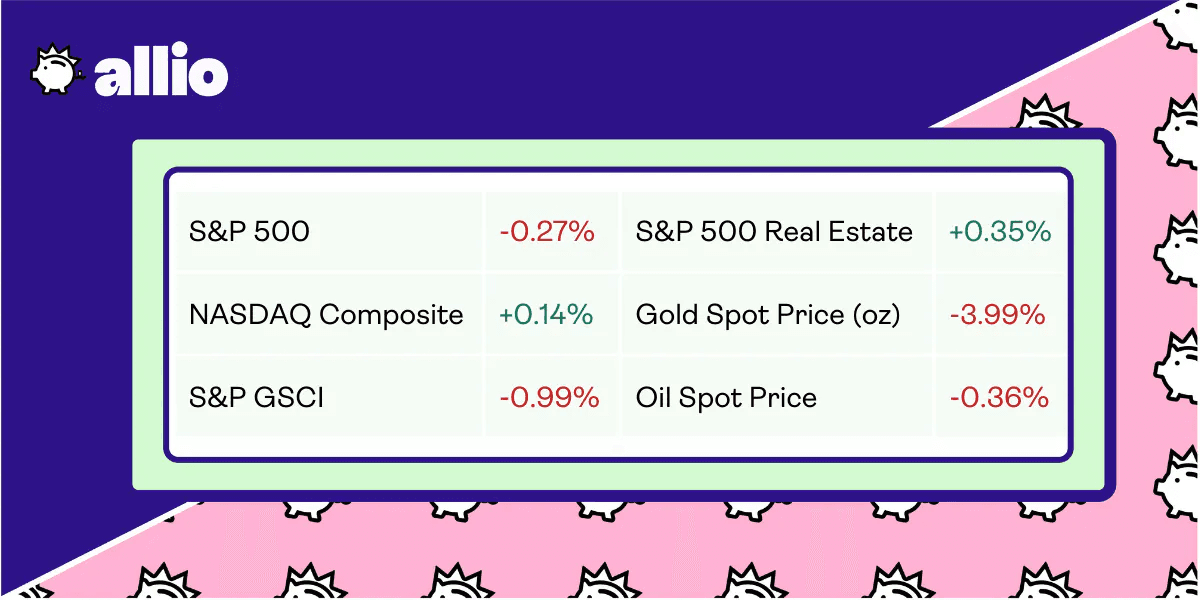

📈 The September swoon continued this week with the broad market losing half a percent, as interest rates and the dollar climbed higher.

💼Economic News

The official cost-of-living adjustment for Social Security will be released in October. Early projections by the Senior Citizens League predict that the rate — also known as the COLA — will be around 3.2%. The average $1,800 check will thus receive roughly a $60 bump. While it may seem a letdown after last year’s 8.7% bump, the rate may be a positive sign of inflation slowing down.

Meanwhile, in the housing market, applications for mortgages to purchase homes are down 2%, compared to 27% during this time last year. This is primarily due to the increase in interest rates, which in turn has resulted in higher mortgage costs.

👀 What to Be on the Lookout for This Week

There are a few economic updates to keep your eye on:

Monday: ISM manufacturing PMI

Tuesday: JOLTs job openings, IBD/TIPP Economic Optimism

Wednesday: ISM services PMI

Thursday: US balance of trade

Friday: Unemployment rate

Additionally, here are companies reporting earnings this week:

Monday: McCormick & Company

Tuesday: Cal-Maine Foods

Wednesday: Acuity Brands, Accolade Brands,

Thursday: Conagra Foods, Constellation Brands, Levi Strauss

📰 In Other News

Negotiators for the Writers Guild of America and the Alliance of Motion Picture and Television Producers have reached a three-year agreement to end the 146-day strike.

According to the WGA, the deal's total value was approximately $233 million — a significant improvement on the initial offer of $86 million. Additionally, the new deal will include restrictions on the use of AI, minimum staffing requirements in television writers' rooms, and a viewership-based streaming bonus.

Meanwhile, Amazon has come under even more scrutiny from the Federal Trade Commission for potentially monopolistic behavior. The FTC filed a massive antitrust lawsuit, alleging that the world’s largest e-commerce store has been exploiting its scale to stamp out competitors. The agency has accused Amazon of penalizing sellers who offer lower-priced products on other platforms, restricting some vendors from Prime shipping benefits, and producing biased search results favoring its own products.

Amazon, however, is sticking to its guns, stating, “The lawsuit filed by the FTC today is wrong on the facts and the law, and we look forward to making that case in court.”

Reflects performance at market close 9/29/23

YOUR ECONOMY

💒Younger Couples Are Securing Love With Prenups

Breaking the Money Mold

It turns out the stars really are just like us. Prenups, once reserved for the rich and famous, are increasing in popularity among all Americans.

A prenup, or prenuptial agreement, is a contract signed before marriage. The agreement lists each person's assets and debts, and outlines how they'll be handled, should the couple part ways.

Traditionally, this type of financial agreement has been closely associated with celebrity marriages, where partners may be high-net-worth individuals with massive estates requiring protection. Celebrity marriages have also statistically been shown to be short-lived, and both parties are keen to protect their often-ample assets. Still, prenuptial agreements used to be fairly rare for the average American couple.

At one point, asking a partner to sign a prenup might have been interpreted as a sign that there wasn't enough faith in the marriage. But, as the saying goes, hope for the best, but prepare for the worst.

Prenup Popularity

At the moment, only 20% of US adults have a prenuptial agreement in place, but more than half say they are open to the idea. This rate is up from last year when only 42% of adults were in support of a prenup.

Moreover, while prenups have traditionally been used by wealthier men, the arrangement is starting to gain popularity with women as well.

Part of the reason prenups are gaining popularity is that couples are marrying later in life. Singles are likely to have amassed more assets by the time they get married. These assets could range from a business, a house, or just a large bank or investment account. If one member of the marriage has anything that they want to protect, they may want to put a prenup in place.

Financial Foresight

Another likely cause for the surge in prenups might not have to do with assets at all, but rather, debt.

Signing a prenup can be an effective way to protect oneself against a partner's debt. In the past, many found themselves paying off a partner’s debt during a divorce, even if they did not know of it before marriage. This is especially important for young couples as the average college graduate has roughly $37,000 in student loan debt.

On a positive note, prenups are very flexible. They can be designed differently to fit a couple's assets, debt, and beliefs. Legally, a prenup can be seen as a way of pre-establishing which assets are personal and which are communal if the marriage ends in divorce. By establishing this beforehand, couples can avoid spending time and money in courts down the road.

Nonetheless, the topic can still be tricky for couples to navigate. It is worth considering speaking to a professional if the decision to sign a prenup is made.

🛑 Gen Z & Millennials Are Reaching Financial Independence Later

Financially Dependent

Millennials and Gen Z are supporting themselves financially much later in life when compared to their parents.

According to a survey conducted by Savings.com, roughly 50% of parents said they support an adult child financially. These parents are sending an average of $1,442 per month to their children, with more than half of them falling into the 20-24 age group.

This financial assistance isn’t being spent on vacations or expensive car payments. Instead, parents are helping their kids pay for basic necessities. Over 75% of parents surveyed said they support a child with their grocery bill, while 56% send money to help with the rent.

This raises the question: Why do Millennials and Gen Z need so much financial assistance?

An Uphill Battle

In the past two years, the United States has experienced some of the worst inflation in decades.

In 2022, basic items like eggs (+59.9%), fuel oil (+41.5%), and butter (+31.4%) all experienced double-digit price hikes. As these increases ripple across everyday essentials, it removes any wiggle room that consumers had in their budget.

This dramatic rise in inflation was only the most recent financial challenge for younger generations. Gen Z and Millennials have also had to grapple with the rapidly increasing costs of college and housing.

In 1980, the cost of a four-year private university was just $3,617 per year. A student enrolling in 2023 will have to pay over $32,000. The same goes for housing. In 1980, median rent was $243. In 2023, the average rent was just over $1,000. In 1980, an 18-year-old could pay roughly $4,000 and receive a full year of college education. Today, one month's rent in a studio apartment in NYC is reaching $4,000.

This rise in prices is to be expected as inflation is a common side effect of the current economic trends. The Federal Reserve aims for roughly 2% to 3% inflation each year, and this has contributed to a significant increase in rent and college over the past forty years. A more pressing issue is that wages have not risen at the same level to keep pace with the rising cost of living.

According to the Economic Policy Institute, middle-wage workers’ real hourly wages have risen just 6% since 1979, while low-wage workers’ wages are down 5%.

Setting Boundaries

There’s no denying that upcoming generations are facing an uphill battle financially. The situation is worsened as most parents are facing financial challenges themselves.

Parents who provide financial assistance to an adult child have found it challenging to discuss reducing these payments. Some experts suggest considering a plan to gradually reduce the assistance over time. For instance, parents currently sending $1,000 per month could continue with this amount for a few months before gradually lowering it to $750, then $500, and so forth.

While it may seem like a complex decision, experts advise that scaling back financial assistance will prove to be a prudent move in the long run — particularly if supporting children financially is straining their own budget and retirement plans.

POCKET CHANGE

Accountants and auditors have been leaving the industry in droves. Most professionals cite low salaries, boring work, burnout, and the threat of generative AI as their main reasons for leaving.

Netflix is sending its last DVD this month, finally sunsetting its original business. Before pioneering streaming, Netflix upended the DVD rental industry by sending movies through the mail.

Many fast food companies are facing class action lawsuits for running ads that misrepresent what their food looks like. A few companies facing these suits include Taco Bell, Wendy’s, McDonald’s, Burger King, and Arby’s.

Credit card companies are racking up losses at the fastest pace since the Great Recession. Goldman Sachs predicts that losses will continue to climb through 2024 and even into 2025.

Amazon is investing up to $4 billion in generative AI startup Anthropic. As part of the deal, the startup will use Amazon Web Services and Amazon’s chips to power its tech.

Head to the app store and download Allio today to start building wealth on autopilot!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.