Updated August 1, 2023

Raymond Micaletti, Ph.D.

Alpha

Equity markets rallied strongly in a data-heavy week last week with the S&P 500 adding 1% and the Nasdaq 100 adding 2%.

Unlike in previous weeks, however, many other segments of the market joined the party, with small caps up 1%, commodities up 3%, and emerging markets up 4%.

The focal points of last week were the Federal Reserve’s policy announcement on Wednesday and mega-cap tech earnings spread throughout the week.

The Fed’s rate hike on Wednesday had been widely telegraphed and the markets’ reaction to the quarter-point hike was muted. Based on Fed fund futures pricing, the market now expects no more rate hikes this year.

Mega-cap tech earnings were also largely well-received–with Google and Meta rising after earnings, and Microsoft falling.

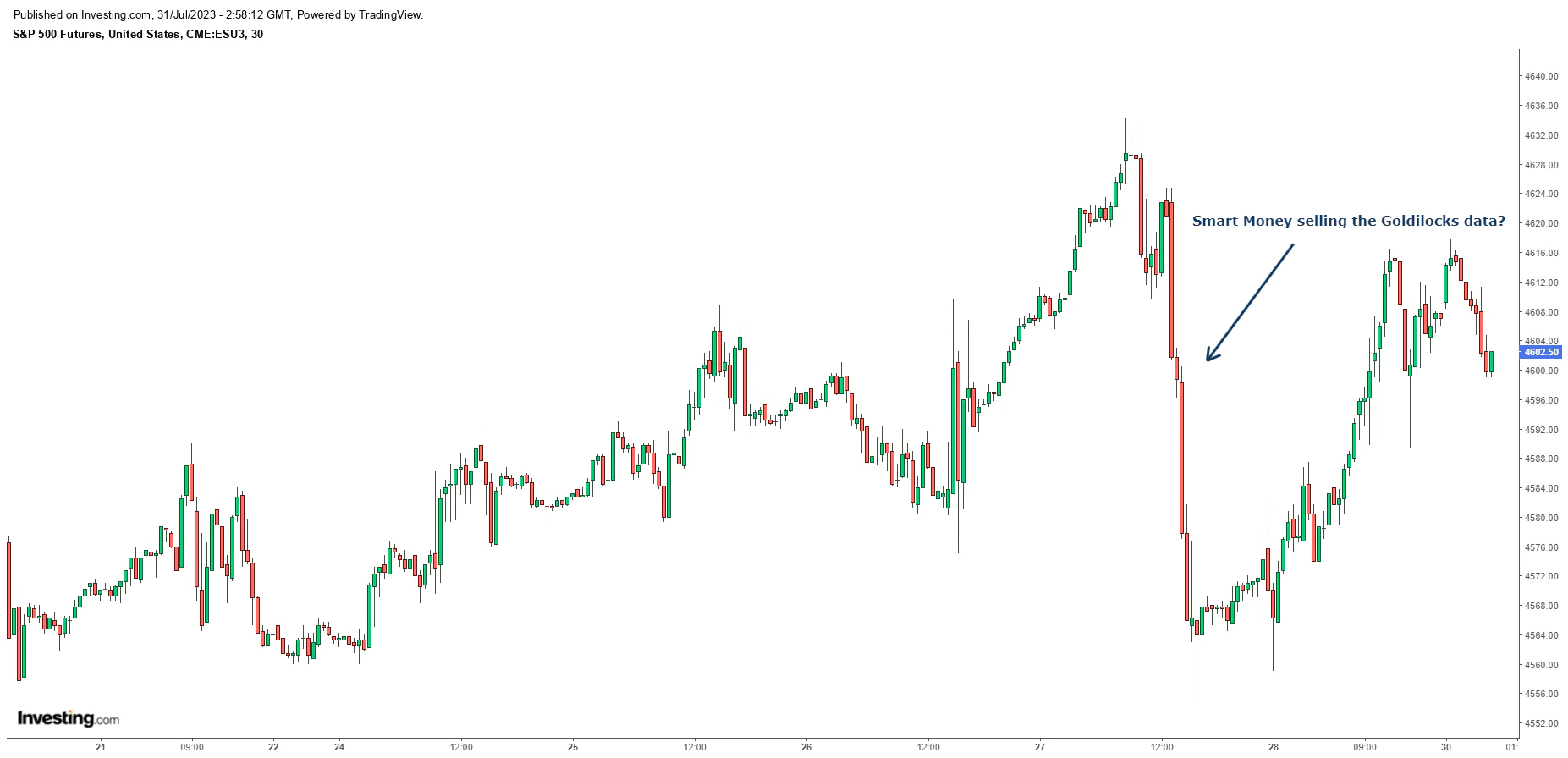

The real fireworks happened on Thursday, however, as we got reports on Q2 GDP, the GDP price index, durable goods orders, wholesale inventories, the U.S. trade balance, and initial jobless claims.

Those reports all came in better than expected. Growth was higher, inflation lower; the trade deficit down, durable goods up; inventories fell while the job market held steady.

The headline numbers were so good that one couldn’t help but think we may have just seen Peak Goldilocks. Acceptance of the soft-landing narrative is now officially mainstream as The Wall Street Journal, The Financial Times, and The New York Times all wrote about its arrival this weekend.

On the heels of that data, coupled with Meta’s earnings the night before, the market raced upwards of 1% higher out of the gate Thursday morning…only to hit a brick wall and finish the day down nearly 1%.

Source: Investing.com

What happened?

The proximate cause was reported to be the market’s fear that the Bank of Japan would be overly hawkish in its adjustments to its Yield Curve Control policy when it met later that day.

That indeed may have been the case, because after those fears were assuaged later that evening, the market rallied strongly on Friday to close the week.

Another interpretation, however, is that the Smart Money looked at Thursday’s data, realized the numbers are probably only going to get worse from here, and sold into those equity market highs.

As Edward Jensen wrote in his 1967 book, Stock Market Blueprints:

“To put it more bluntly, mass money [i.e., institutions] absolutely needs bad news and discouraging events to get mass people [i.e., retail traders] to sell their stocks. Now it should not require a Ph.D. degree to figure out what conditions must be necessary when mass money wants to sell their holdings… Every emotion makes you want to buy and certainly the news is nothing but good.

If things are that good, then what rational man would sell his stock? Mass money who bought some time earlier must have good news and events in order to find buyers for their stock. Mass money is more likely to buy closer to the bottom than to sell right at the top. Since stocks come down generally faster than they go up, mass money will usually begin selling before the final top is reached and will keep selling even into the early states of the next downtrend.”

If you’ve been reading this newsletter the past 12 months, you’ll recall that institutions were buying stocks starting in late June 2022 (when most stocks bottomed) and were backing up the truck in October when the prevailing narrative was at its most bearish.

Recently, however, institutions have been selling as the market has continued to rise. Almost certainly they used Thursday’s good news to unload more of the stock they had bought at much lower prices.

Why do we think the news will only get worse from here for the soft-landing narrative? Simply put, commodities.

Broad commodities are up nearly 12% since late June. Oil is up 18%, and gasoline is up 22% in that time. Demand for oil and gasoline is poised to set records–see here, here, here, and here–while at the same time there appears to be a two-million-barrels-per-day deficit in the oil supply (and gasoline reserves are at a 5-year low for this time of year).

Source: Investing.com

As all goods need to be shipped using either diesel or gasoline, the price of everything else will likely rise in conjunction.

As last week the market a) priced in no more Fed hikes and b) priced in higher long-term bond yields, the market might also be suggesting a resurgence of inflation (which would reduce the attractiveness of long-duration bonds).

Now, getting the macro right isn’t easy, especially when things are obvious.

It was obvious last year that a recession was coming.

It was obvious last year that the S&P was going to 3200.

It’s obvious now that inflation is set to perk up.

Or is it?

We can’t say with certainty. So instead, we’ll look to see how the Smart Money is positioning themselves.

Last week, the Smart Money sold the dollar (hard), bought gold, silver, and crude oil, and turned relatively bearish on the headline equity indices (S&P 500, Nasdaq 100, Russell 2000) based on cross-asset positioning in growth- and inflation-related assets.

That type of action seems to corroborate the idea that inflation is set to reappear in the not-too-distant future.

To be fair, however, dollar relative sentiment is still flirting with turning bullish and the dollar did rally back above its breakdown level from the week prior.

Moreover, while growth-and-inflation-related relative sentiment did turn bearish for headline equity indices, our overall measure of relative sentiment is still marginally bullish for equities.

And despite the Smart Money having bought gold, silver, and crude oil last week, their relative positioning in those assets still leans neutral or bearish.

Thus, if inflation does reappear, it may be a gradual reawakening rather than an immediate spike higher.

Let’s examine the bull and bear cases for equities.

The Bull Case

The bull case is largely unchanged from last week and consists of positive momentum, mega-cap tech being in a nascent bubble, election season on the way, and peak housing pain likely being behind us.

To those points we would add:

Another breadth thrust: The S&P 500 registered another breadth thrust this past week with 70% of stocks above their 200-day moving average, 80% above their 20-day moving average, and 80% having spent at least 10 days above their 50-day moving average. Twenty of 21 instances finished positive one-year forward with an average return of 15%. This is at least the third breadth thrust in the past seven months and given their historical performance, they should be respected.

BTFP liquidity keeps rising: The program the Fed instituted to shepherd the banks through the bank crisis earlier this year continues to lend out money and the equity market has followed the trajectory of that lending higher.

The Bear Case

The bear case is also largely unchanged from last week, clocking in with:

Cross-asset relative sentiment in the headline equity indices has turned bearish

Extreme retail sentiment (and now fund manager sentiment, too)

Stretched equity positioning amongst hedge funds

Tech stock seasonality

The AI narrative might be more hype and hope than substance

The dollar refuses to die

To those points we would add:

Bubbling inflation: Inflation looks set to reemerge in the coming weeks and months based on commodities recent performance coupled with record oil demand (and a 2-million-barrel-per-day supply deficit)

Repellent valuations: The difference between expected annualized 10-year U.S. equity returns and the 10-year U.S. Treasury yield is now -200 basis points–indicating long-term unattractiveness of U.S. equities relative to nominal bonds, which themselves are unattractive due to the negative real yields they will generate

Our View

As perfect as the economic and earnings data were last week, it’s reasonable to believe we have reached Peak Goldilocks. In other words, will the data, and particularly the inflation data, be getting better or worse from here?

In light of the recent surge in commodities and the apparent strong demand for oil and gasoline, it would appear that things can only get worse on the inflation front.

Throw in the fact the smart money sold the dollar, bought gold, silver, and crude oil last week while also remaining resolutely bullish in several inflation-sensitive segments of the market and it appears as though inflation is not quite dead and buried just yet.

And although cross-asset relative sentiment is still bullish in certain inflation-sensitive areas of the market, it has now turned bearish in the headline indices (S&P 500, Nasdaq 100, developed markets, emerging markets). Moreover, inflows to tech stocks are the antithesis of what they were in late 2022–tech is a crowded trade now–and equity indices are running up against resistance with obvious bearish divergences in their technical momentum.

Thus, if the market does continue higher–and over the intermediate-term we suspect it will (as it pays to respect the recent breadth thrusts)–we would expect the leadership of the rally to change from technology to other sectors.

But, given the magnitude of the four-month straight-up rally we have just witnessed, we could just as easily see a pullback of some sort in the near-term, or at the very least some sideways churn to consolidate recent gains.

If we are fortunate enough to get a pullback in equities, said pullback would likely represent a solid buying opportunity so long as it’s not accompanied by an exogenous shock or strongly bearish positioning on the part of the Smart Money.

Conversely, if the market continues marching higher from here at the same pace it has over the last several months, it would likely only be setting itself up for a quick, violent decline at a not-too-distant later date, as institutions no doubt will continue selling into the rally.

Allio Portfolio Updates

No change to Allio’s core portfolio last week. However, we did use the Thursday selloff to take tactical positions in Apple and Microsoft, largely to hedge upside risk if mega-cap tech continues to rise and also because those names should hold up better if the market pulls back in the near-term.

Want access to your own expert-managed investment portfolio? Download Allio in the app store today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.