Updated June 13, 2023

Raymond Micaletti, Ph.D.

Macro Money Monitor

Market Recap

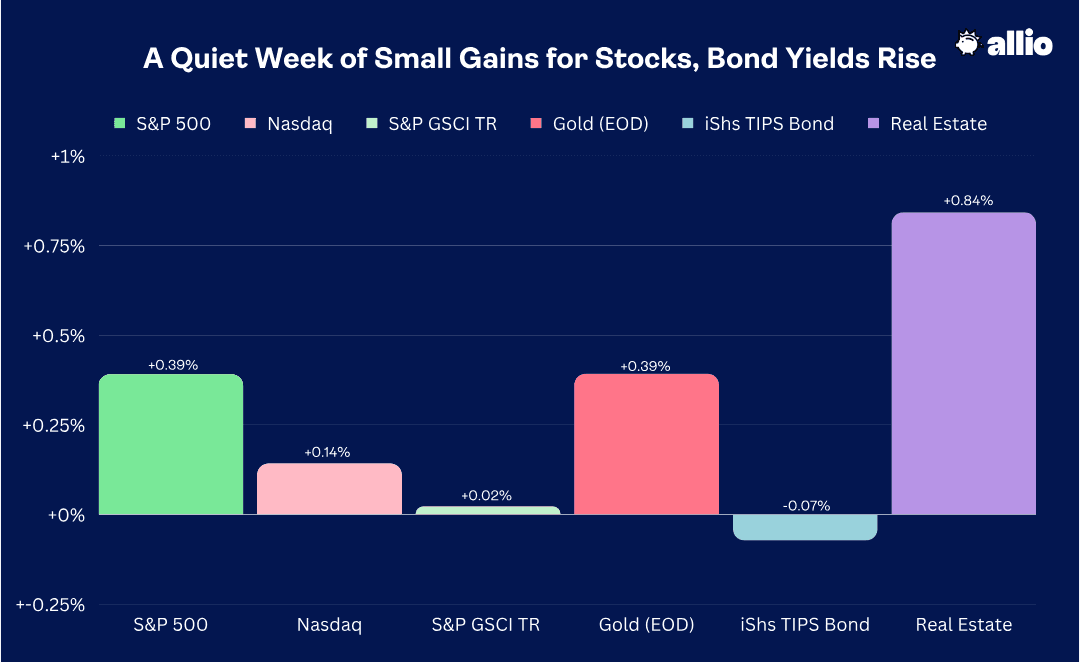

The S&P 500 crept higher by 0.4% last week amid a light-volume stretch before this week’s key Fed rate decision. Small caps outperformed while the NASDAQ Composite finished just fractionally in the black – good for its seventh consecutive weekly advance.

The Real Estate sector posted a gain just shy of 1% as some cyclical niches of the market gained ground on the mega-caps. Commodities, meanwhile, were roughly flat despite some intra-week volatility around headlines out of Saudi Arabia and other OPEC+ nations regarding the supply of oil. Lastly, gold continues to meander under the $2,000 per ounce level but managed to rally for the week.

June 2, 2023 - June 9, 2023

It was a classic summer-like stretch on Wall Street. While the solstice happens next week, plenty of traders appeared to have taken time away from their screens to soak up the sun. Perhaps their beach plans were disrupted by the great New York Smoke Out last Thursday. Nevertheless, volumes were light last week, and volatility was subdued.

The CBOE VIX Index dipped to its lowest level since February of 2020 – pre-pandemic – while other measures of market anxiety were muted. As we scan the asset classes, a cloud of calmness has been ushered in across large and small-cap equities, foreign exchange markets, and even the oil patch. But are investors too relaxed? Let’s cut through the haze with some key indicators and what they suggest.

Behold, A Bull Market Is Born (Really?)

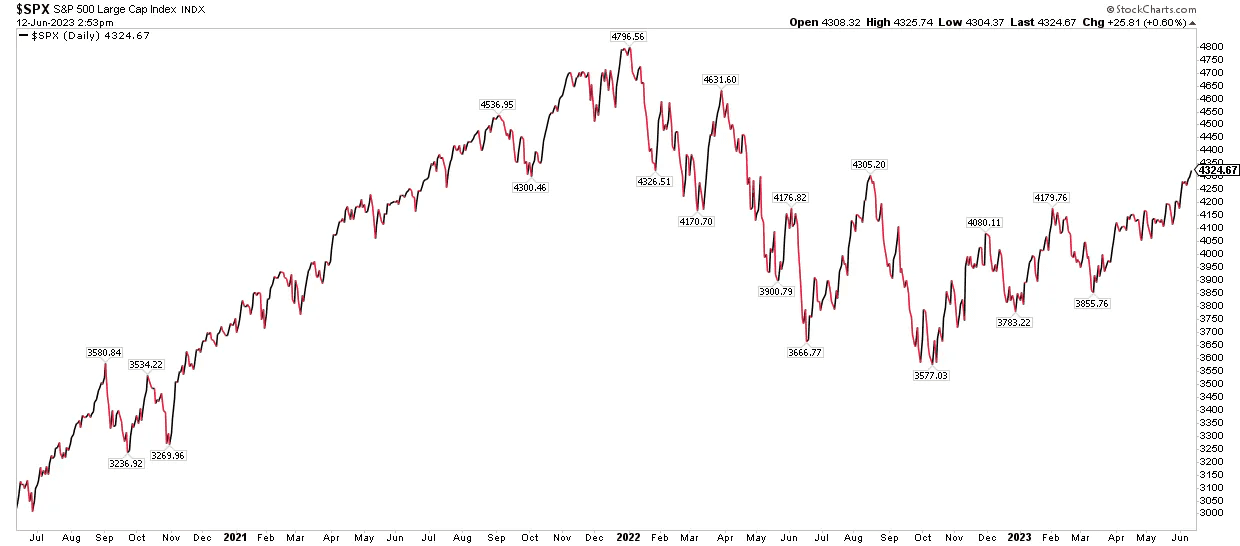

First, technicians and TV commentators alike rejoiced this past Thursday. The S&P 500, at long last, climbed to a 20% rally off the closing low some eight months ago. October 12, 2022, marked the nadir, and at the time, it indeed felt like the world was burning. Following a hot CPI report for September, yields jumped, and investors had to come to grips with the reality that the Fed would have to accelerate its rate-hiking initiative.

Pessimism reached a peak, though, and yields soon backed off. The bid to bonds helped the SPX stage a Q4 rally, led by value sectors and cyclical industries. The new year then brought a new round of leadership. While areas like banks, oil & gas companies, and the Industrials sector outperformed in 2022, mega-cap tech began their meteoric ascent. Apple, Microsoft, Amazon, NVIDIA, Google, Tesla, and Meta have been dubbed the “Magnificent Seven,” as we detailed last week. And a sharp rise in shares of Netflix lately might make the new moniker the “Elite Eight.” But will markets soon be on cloud nine care of new leadership?

S&P 500 Rallies 20% Off Its October 2022 Low

Source: Stockcharts.com

Strategists left and right have been waiting for a breadth expansion. While data show it's not inherently bearish for equities to be led by a handful of the biggest companies, there’s a better feeling about the vigor of a bull market when so-called “risk-on” assets like small and mid-caps participate. June has brought about a shift in leadership.

So far on the month, the Russell 2000 small-cap index is up almost 7% while large caps are higher by just 3%. The Nasdaq 100 ETF (QQQ) has been the underperformer – rallying less than 2% thus far in June. And last week was the clearest tell of all. Micro-caps led the way while mega-caps produced the worst alpha. But will the trend continue?

Allio’s Stance

We are increasingly skeptical that the rally can continue – particularly in tech. Once we spotted emerging relative weakness in the Nasdaq 100 ETF, we cut our position there in half. That portfolio action aligns with our view that the year-to-date performance gap between the “Qs” and the SPX is simply too large, and that some mean reversion should ensue.

Thus, we wouldn’t be surprised to witness a cooling-off period in some of the major indices – particularly among the major tech-dominated ones. Still, a modest melt-up will likely take place, but seasonality suggests that the second half of June is wont to feature a small give-back of gains. The ever-bullish pre-election year may keep a bid to stocks, though.

Stock Market Seasonality: Neutral Ahead of Mid-Year

Source: Stock Traders’ Almanac

Brace for an Onslaught of Economic Data & Central Bank Hoopla

While the technicals are fascinating right now and as the financial media debates what determines a true bull market, this week promises to be more eventful than last week’s tranquility. The docket is full.

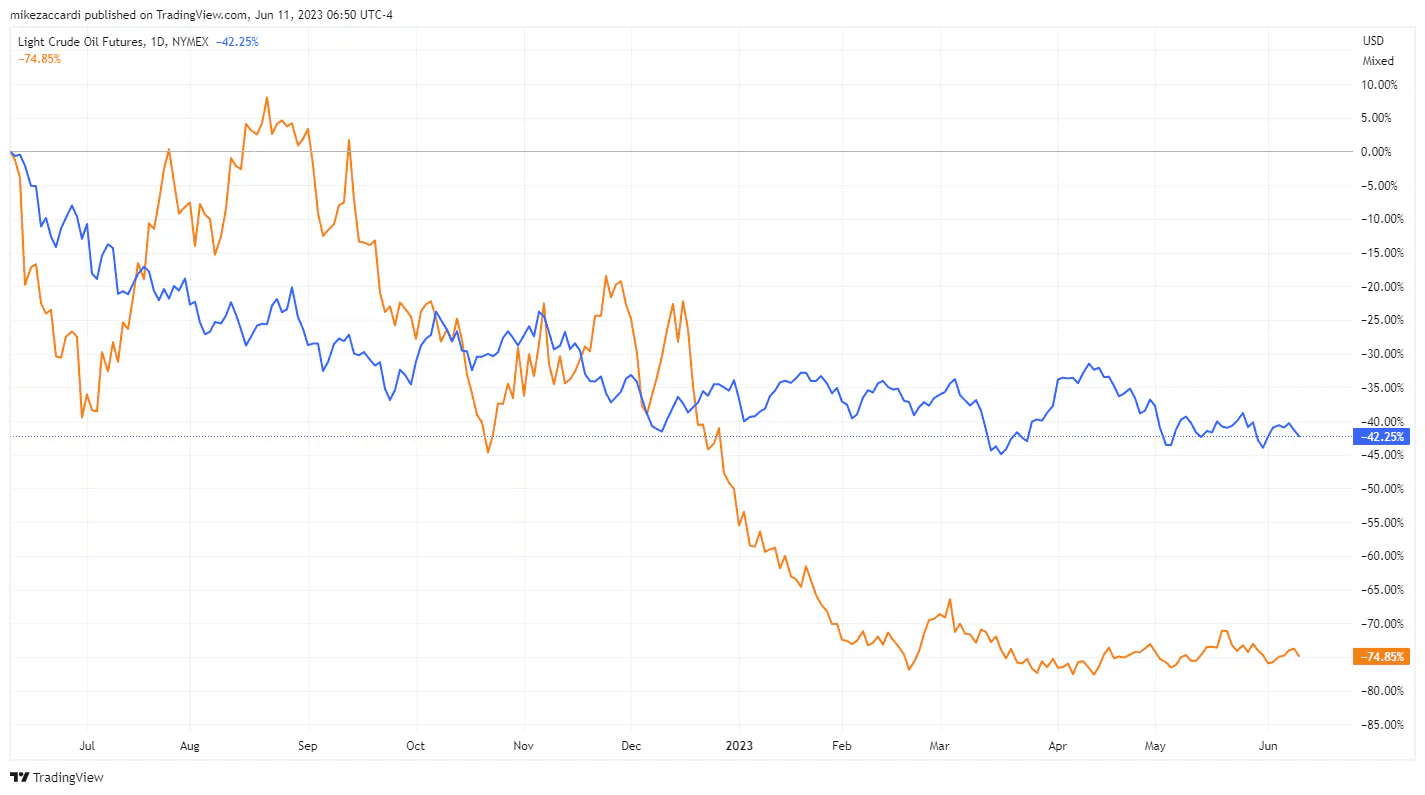

First, Tuesday’s May CPI data will of course impact markets. The curveball with inflation readings for last month and June is that it was this time a year ago when energy prices reached their climax. In the USA, the cost of a gallon of regular at the pump had soared to the $5 level.

Today, however, the national average gas price is near $3.60. Likewise, WTI crude oil has moved from above $120 to near $70, a roughly 40% fall off. Natural gas has also crashed, to put it bluntly. So, the Headline CPI rate on a year-on-year basis will appear to be on the right path.

Oil & Gas Prices Plunge YoY, Helping the Headline CPI Rate to Retreat

Source: TradingView

As it stands, economists expect a 4.1% Headline CPI rate while Core CPI (ex-food and energy) is seen as falling from 5.5% through April to 5.3% as of last month. Moreover, the UN reports that the FAO Food Price Index fell in May and is down about 20% from a year ago.

But the devil might lurk in the month-on-month Core rate – the consensus calls for a 0.4% rise. That is still uncomfortably high for FOMC members. Chair Powell and the rest of the Fed will once again pay close attention to the ‘core services ex-housing' figure within the CPI report.

A Slew of Key Macro Events Tuesday Through Friday This Week

Source: BofA Global Research

Another indicator suggesting that inflation is on the mend is domestic rent prices. Redfin reports that the annual change in the cost to rent an apartment in the US has turned negative for the first time since early 2020. Most of the weakness is seen in the West region while hot markets persist along the sunbelt.

A danger for the Fed on Wednesday, should they hike rates, is that additional tightening of credit conditions could further harm the fragile real estate market.

Rental Market Deflation

Source: Redfin

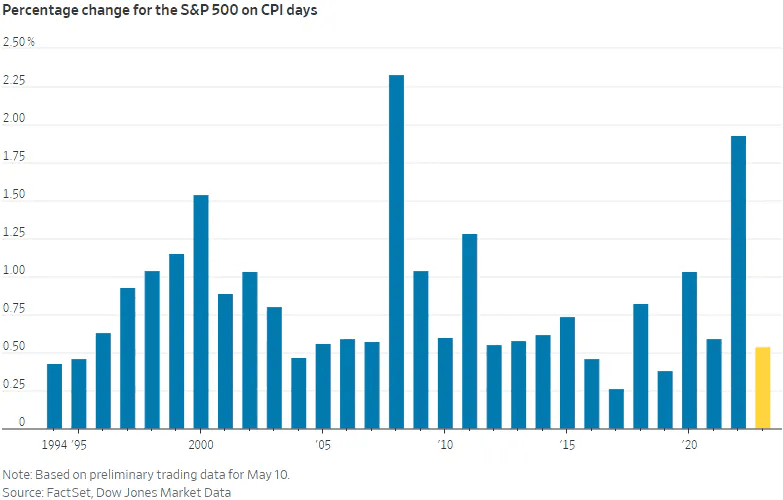

But we might not see fireworks this Tuesday on the NYSE. Equities have largely looked past the CPI report in 2023. The average price change on CPI days is a smidgen more than 0.5% so far this year. Contrast that to the monster drops and rallies of 2022 in which the S&P 500 averaged a change of nearly 2%.

It’s clearly a different environment, and investors recognize that the monthly inflation gauge is backward-looking, and more emphasis should be placed on how the Fed reacts to all the incoming data.

Muted Stock Market Moves Post-CPI in 2023

Source: The Wall Street Journal

So maybe the Wednesday afternoon Fed decision should be in the spotlight rather than Tuesday morning’s CPI news. Busting out one of our favorite macro charts, the CME’s FedWatch Tool shows an unusual picture of Fed rate expectations. Significant uncertainty remains as to what Powell and the gang will do - there’s a 70% chance of a skip, but a still-elevated 30% probability of a policy rate increase.

Usually, once we are this close to the decision date, rate traders have made up their minds. Or, as has sometimes been the case lately, WSJ’s Nick Timiraos (the “Fed Whisperer”) will have essentially leaked the news. Whatever the outcome, the Fed’s terminal rate has been steady near 5.3% after jumping back up in April and May following a dip during the regional banking crisis.

Monetary policy drama is not confined to the US Federal Reserve. On Thursday, the European Central Bank gathers, and then Japan’s BoJ issues its new policy on Friday. Expect some volatility in the fixed-income and foreign exchange markets.

Keeping with the overseas theme, key data out of China on Thursday will shed new light on the world’s second-largest economy’s recovery following a tepid reopening this year. Data on new home prices, unemployment, industrial production, and retail sales all hits on Thursday. Stocks related to China’s real estate market have caught a bid lately amid inklings of a stimulus package targeted at that economic sore spot.

Turning back stateside, regional surveys will offer clues on just how badly the manufacturing slice of the domestic economy is fairing. Empire Manufacturing and the Philly Fed probably won’t paint rosy pictures on Thursday. The bulls hope that robust Retail Sales for May will support the soft-landing narrative.

As inflation eases and with a robust jobs market, there are growing signals that the Fed can indeed pilot a gradual easing of GDP growth rather than inflicting a painful recession on consumers. This week could upend that sanguine narrative should CPI come in hot and retail sales disappoint amid steeply contractionary regional manufacturing data.

Retail Sales Read: Card Spending Was Generally Solid in May, Says BofA

Source: BofA Global Research

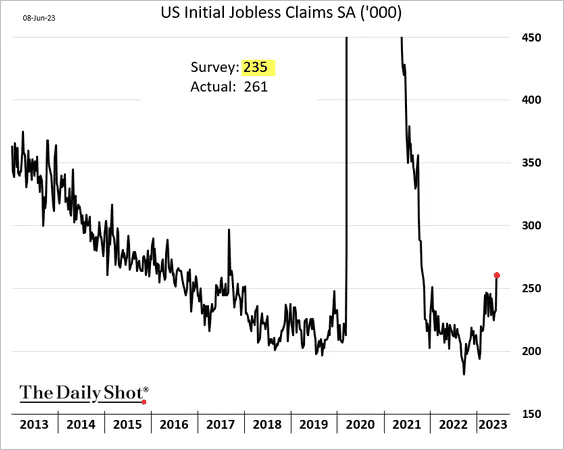

And don’t discount the impact of Thursday morning’s Jobless Claims report. Last week, a surprising jump in initial claims stirred up fears about the beginning of labor market woes. The bigger-than-forecast weekly figure came on the heels of a hot May NFP employment report. A single number does not make a trend, though, so if we see confirmation of a spike in claims, then expect bond yields to dip as recession chatter once again heats up.

Initial Jobless Claims Jump to Highs Not Seen Since Late 2021

Source: The Daily Shot

Lastly on the economic front, we get a preliminary read on June consumer sentiment on Friday. The University of Michigan’s monthly survey offers a glimpse of how folks assess the current situation as well as their outlook for the coming months. Key to watch will be feelings on prices – a jump in 1-year or 5-10 year inflation expectations will not help the Fed’s cause.

Stocks Rise, Investors Now Walk with a Swagger

Putting it all together, investors feel pretty upbeat about the state of markets. It has been a while since we’ve touched on the weekly survey of investors from the American Association of Individual Investors (AAII). The reason? It’s been telling the same old bearish story. But, as with Jobless Claims, there was a significant shift last week.

For the first time since December 2021, bulls outnumbered bears by at least 20 percentage points. The “bull-bear” spread was negative for all but a few weeks in 2022 up through last month, but as stocks have risen, investors have turned more hopeful. While not a pure contrarian signal, we can no longer say that the current market rally is hated.

The Bottom Line

We detailed how last week would be a respite for market watchers. Indeed, the VIX moved to its lowest level in years while a dearth of economic data points allowed financial TV to focus on a controversial golf merger and smokey skies over the Northeast. This week is already a bit more active, and bellwether economic reports as well as a trio of central bank policy decisions will keep traders on edge.

Want access to your own expert-managed investment portfolio? Download Allio in the app store today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.